Moneybox – 2025

Bundles

Role: Lead Product DesignerTeam: Product, Analytics, Engineering, ContentImpact: +51–76% uplift in cross-sell

Opportunity

Most Moneybox customers held only one product, despite multi-product customers being materially more valuable.

76.9%

of customers held one product

1.85×

more revenue from customers with a second product

2.25×

higher AUA for multi-product customers

How might we encourage more customers to take a second Moneybox product, earlier in their journey?

Problem

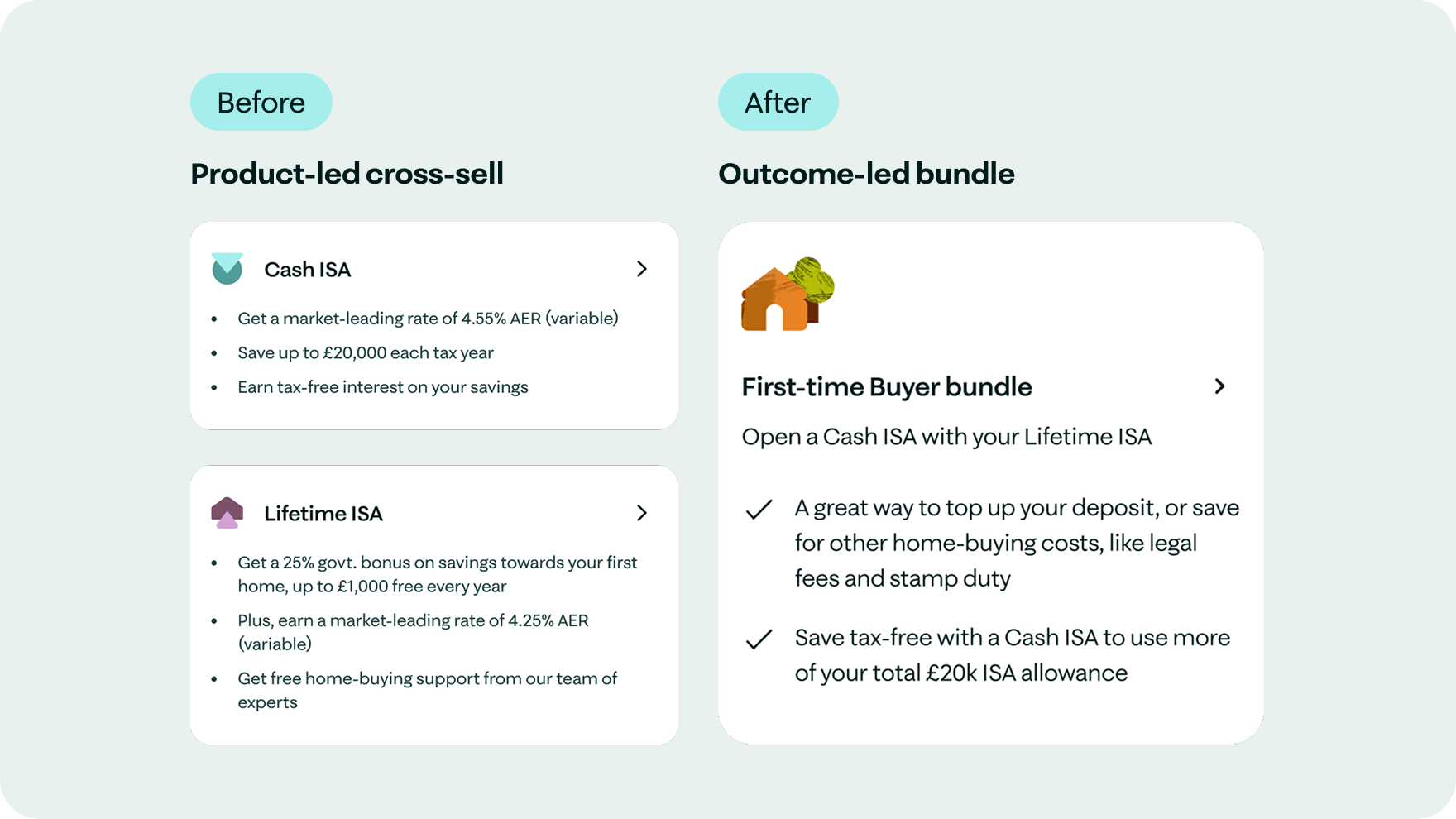

Existing cross-sell journeys largely promoted products in isolation.

Customers could understand what a Cash ISA or Lifetime ISA did individually, but there was little context around why opening a second product could help them make progress towards a broader financial goal.

Insight

Would outcome-led bundles make taking a second product feel more relevant?

We believed customers would be more likely to open a second product if complementary accounts were framed around a shared financial outcome, rather than presented as standalone cross-sell offers.

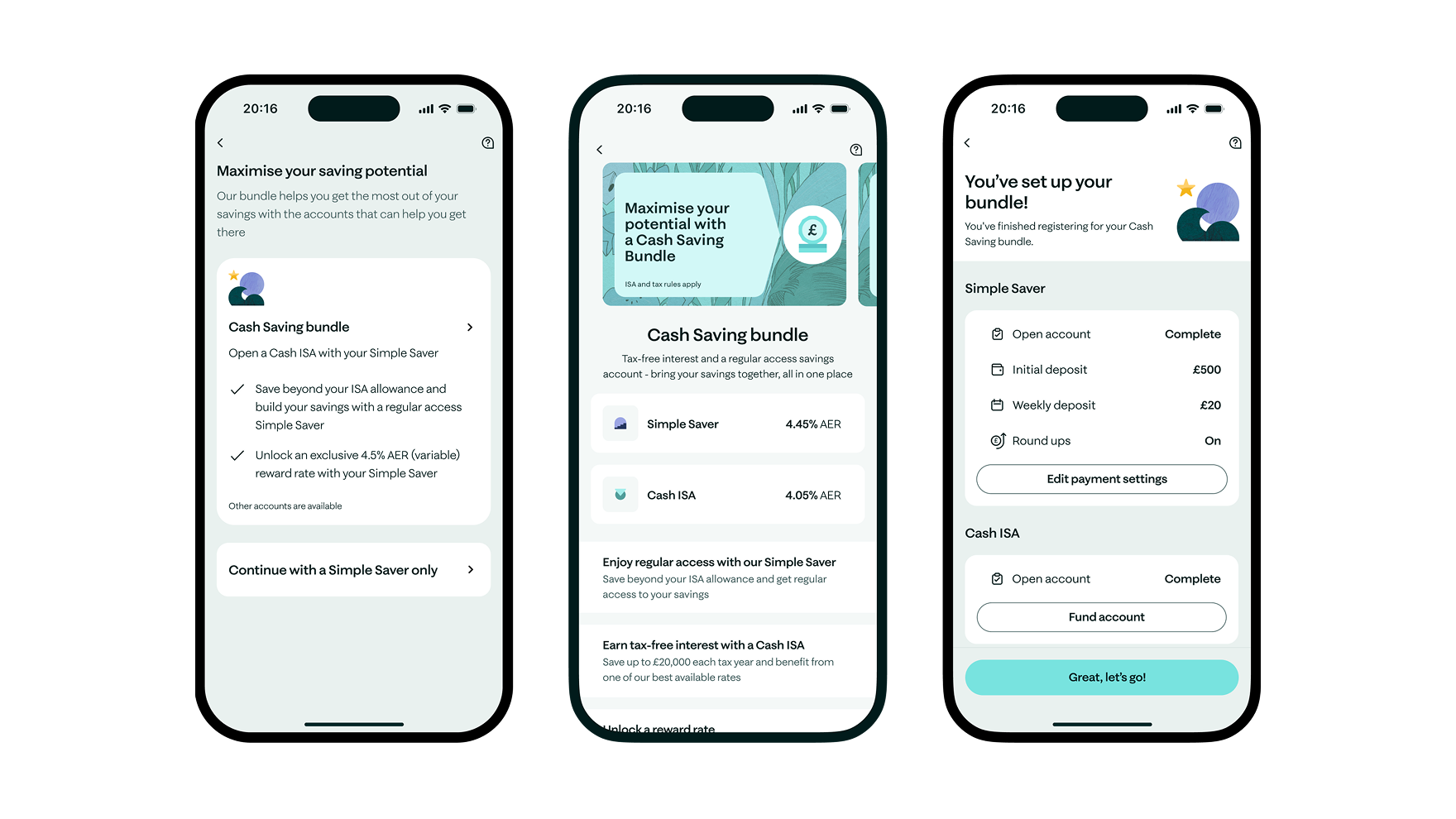

For example, instead of recommending a Cash ISA after someone selected a Lifetime ISA, we introduced a First-time Buyer bundle, positioning it as a way to not only save for your deposit, but for other home-buying costs, such as furniture and fees.

Experimentation & strategy

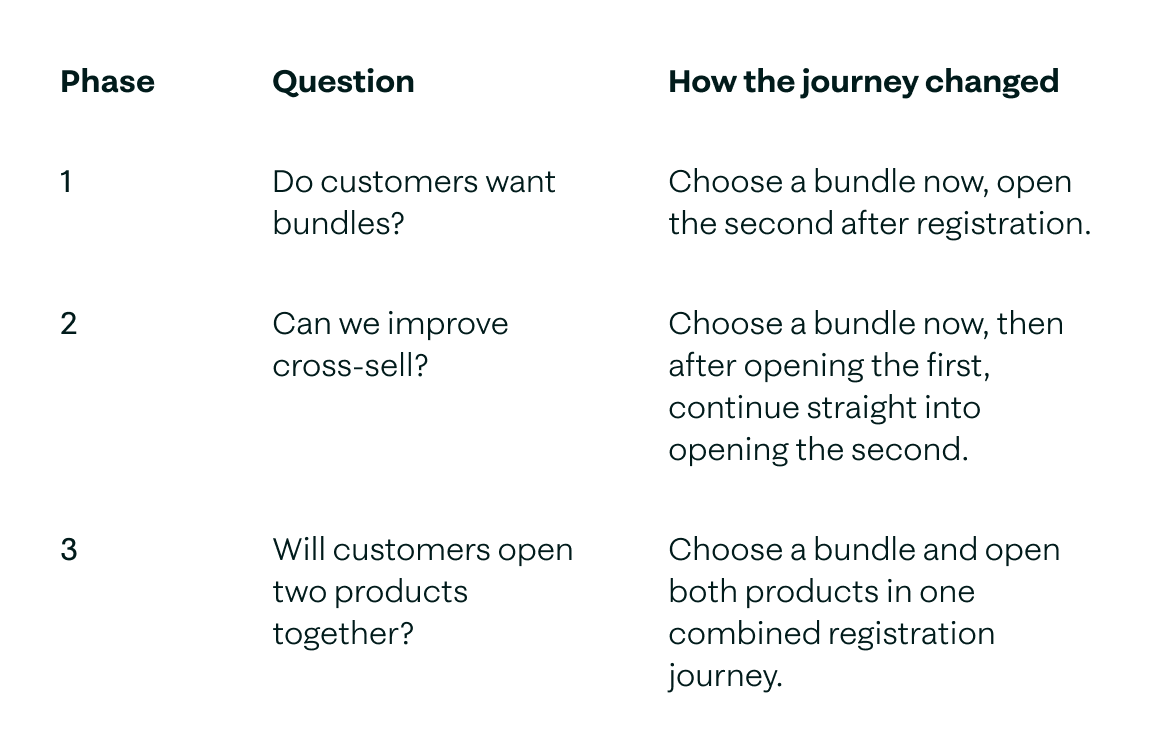

Rather than build a full two-product registration journey upfront, we tested the proposition in three progressive phases.

Each phase answered a different question:

Phase 1

Is there appetite for bundles?

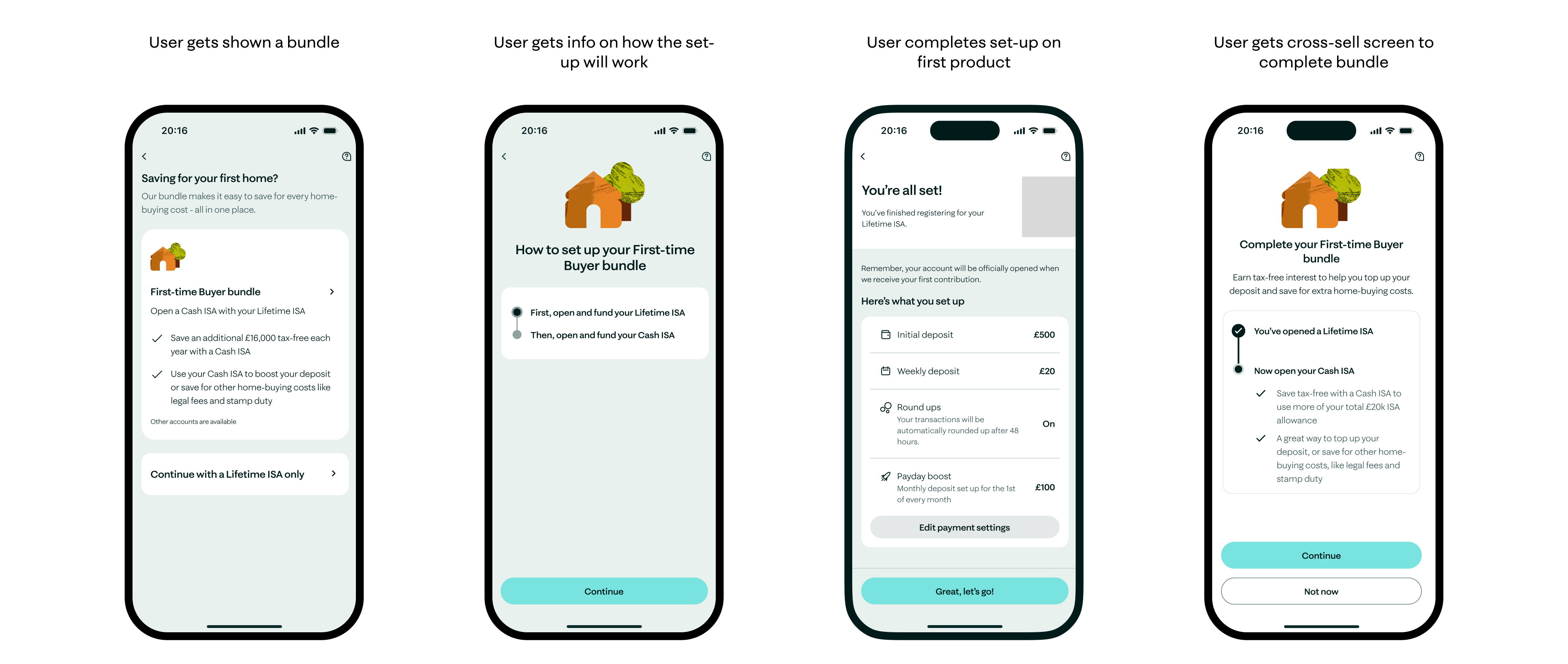

We started with a lightweight fake-door test. This allowed us to validate demand before investing in a more complex registration flow.

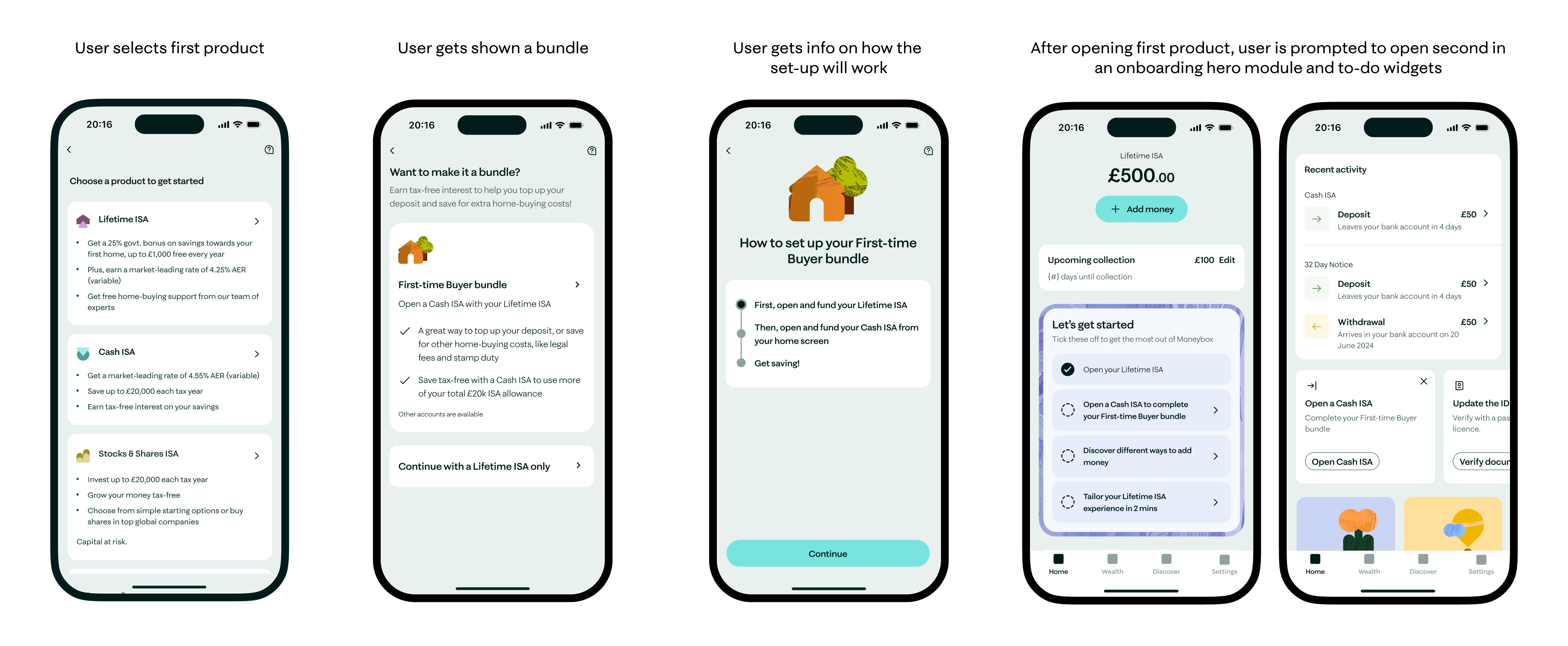

After selecting their first product, customers were offered a relevant complementary bundle. To keep scope low, customers still registered for their original product first. If they chose a bundle, they were prompted to open the second product later through an onboarding hero module.

Results

30%

of customers selected a bundle when shown one

68%

of those customers went on to open the second product post-reg

Learnings

- Customers were open to a second-product recommendation when it was tied to a clear financial outcome.

- We saw early evidence that bundles could influence which second product customers chose. For example, users choosing the First-time Buyer bundle were more likely to open a Cash ISA, whereas users in the control journey more often selected a Simple Saver.

- This was directional rather than statistically significant, but it suggested that outcome-led framing could help customers understand the role of a second product.

Phase 2

Can we improve cross-sell?

Phase 1 proved that people liked bundles, but there was still a break between choosing one and opening the second product.

We introduced a post-registration screen that allowed customers to continue directly into setting up their second product. Customers who skipped could still return later through the onboarding hero.

Results

+1.9 - 3.8%

Cross-sell increase across the bundle journeys.

Learnings

Intent was strongest immediately after customers committed to their first product. Delaying the second-product journey created unnecessary friction.

Phase 3

Will users open two products at once?

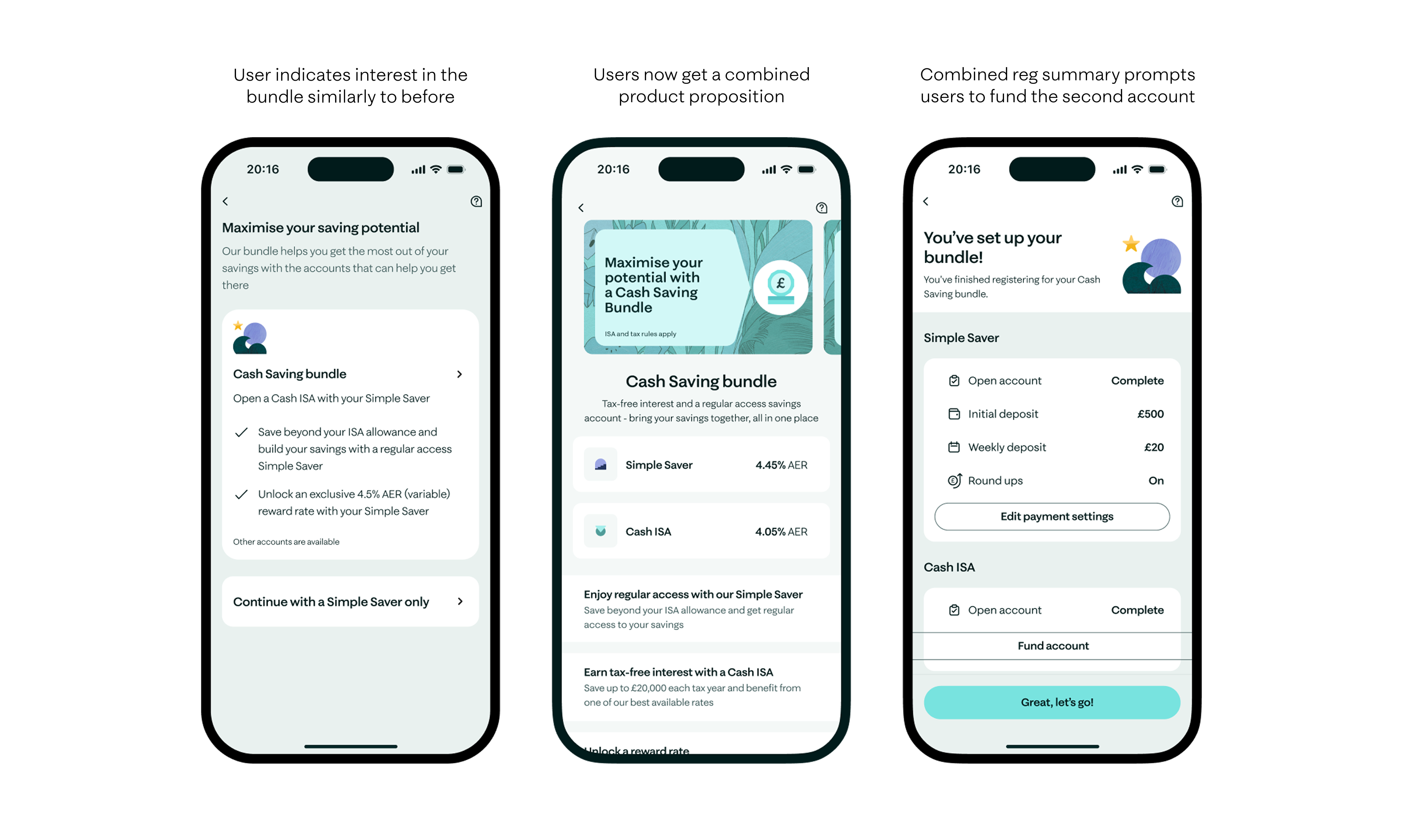

In the final phase, we removed the remaining hand-off.

Customers who chose a bundle saw a combined product-detail experience and completed a streamlined registration journey for both products together.

Technical constraints meant customers could only initially fund one product during registration, then fund the second product immediately after entering the app.

Results

+51.4–76.3%

uplift in cross-sell versus the control journey

That means, for every 1,000 cross-sells in the control journey, Phase 3 generated at least 514 additional cross-sells.

Future phase

Increase second product funding

Phase 3 solved the problem of second-product opening, but second-product funding still lagged behind.

Only 44% of customers funded their second product, compared with around 81% in the control experience. This became the next priority: improving funding without losing the stronger cross-sell performance.

Near-term ideas included an immediate funding prompt and post-registration re-engagement. Longer term ideas explored a connected “fund your bundle” experience that could split a single deposit across both products.

I handed over the opportunity area and early concepts; delivery continued after my involvement.

Outcome

Bundles shifted the team’s approach from product-led cross-sell to outcome-led financial planning.

By helping customers understand how products could work together, and progressively reducing friction in the journey, we proved that users were willing to open two products in one registration flow.

The work created a scalable foundation for increasing multi-product adoption, AUA and long-term customer value.

Get in touch

This website is just a little peek into my work. I’ve got plenty more I’d love to yap about – if you’d like to hear it more, let’s chat!

Moneybox – 2025

Bundles

Role: Lead Product DesignerTeam: Product, Analytics, Engineering, ContentImpact: +51–76% uplift in cross-sell

Opportunity

Most Moneybox customers held only one product, despite multi-product customers being materially more valuable.

76.9%

of customers held one product

1.85×

more revenue from customers with a second product

2.25×

higher AUA for multi-product customers

How might we encourage more customers to take a second Moneybox product, earlier in their journey?

Problem

Existing cross-sell journeys largely promoted products in isolation.

Customers could understand what a Cash ISA or Lifetime ISA did individually, but there was little context around why opening a second product could help them make progress towards a broader financial goal.

Insight

Would outcome-led bundles make taking a second product feel more relevant?

We believed customers would be more likely to open a second product if complementary accounts were framed around a shared financial outcome, rather than presented as standalone cross-sell offers.

For example, instead of recommending a Cash ISA after someone selected a Lifetime ISA, we introduced a First-time Buyer bundle, positioning it as a way to not only save for your deposit, but for other home-buying costs, such as furniture and fees.

Experimentation & strategy

Rather than build a full two-product registration journey upfront, we tested the proposition in three progressive phases.

Each phase answered a different question:

Phase 1

Is there appetite for bundles?

We started with a lightweight fake-door test. This allowed us to validate demand before investing in a more complex registration flow.

After selecting their first product, customers were offered a relevant complementary bundle. To keep scope low, customers still registered for their original product first. If they chose a bundle, they were prompted to open the second product later through an onboarding hero module.

Results

30%

of customers selected a bundle when shown one

68%

of those customers went on to open the second product post-reg

All three bundles drove higher cross-sell than the existing journey.

Learnings

- Customers were open to a second-product recommendation when it was tied to a clear financial outcome.

- We saw early evidence that bundles could influence which second product customers chose. For example, users choosing the First-time Buyer bundle were more likely to open a Cash ISA, whereas users in the control journey more often selected a Simple Saver.

- This was directional rather than statistically significant, but it suggested that outcome-led framing could help customers understand the role of a second product.

Phase 2

Can we improve cross-sell?

Phase 1 proved that people liked bundles, but there was still a break between choosing one and opening the second product.

We introduced a post-registration screen that allowed customers to continue directly into setting up their second product. Customers who skipped could still return later through the onboarding hero.

Results

+1.9 - 3.8%

Cross-sell increase across the bundle journeys

Learnings

Intent was strongest immediately after customers committed to their first product. Delaying the second-product journey created unnecessary friction.

Phase 3

Will users open two products at once?

In the final phase, we removed the remaining hand-off.

Customers who chose a bundle saw a combined product-detail experience and completed a streamlined registration journey for both products together.

Technical constraints meant customers could only initially fund one product during registration, then fund the second product immediately after entering the app.

Results

+51.4–76.3%

Cross-sell increase across the bundle journeys

That means, for every 1,000 cross-sells in the control journey, Phase 3 generated at least 514 additional cross-sells.

Learnings

Customers did not need to be eased into a second product through a separate journey. Once the value of the bundle was clear, they were willing to set up both products in one registration flow.

The biggest remaining barrier was not product opening, but funding: users could open both accounts, but the second product still needed a clearer, more intentional funding journey.

Future phase

Increase second product funding

Phase 3 solved the problem of second-product opening, but second-product funding still lagged behind.

Only 44% of customers funded their second product, compared with around 81% in the control experience. This became the next priority: improving funding without losing the stronger cross-sell performance.

Near-term ideas included an immediate funding prompt and post-registration re-engagement. Longer term ideas explored a connected “fund your bundle” experience that could split a single deposit across both products.

I handed over the opportunity area and early concepts; delivery continued after my involvement.

Outcome

Bundles shifted the team’s approach from product-led cross-sell to outcome-led financial planning.

By helping customers understand how products could work together, and progressively reducing friction in the journey, we proved that users were willing to open two products in one registration flow.

The work created a scalable foundation for increasing multi-product adoption, AUA and long-term customer value.

Get in touch

This website is just a little peek into my work. I’ve got plenty more I’d love to yap about – if you’d like to hear it more, let’s chat!

Moneybox – 2025

Bundles

Role: Lead Product DesignerTeam: Product, Analytics, Engineering, ContentImpact: +51–76% uplift in cross-sell

Opportunity

Most Moneybox customers held only one product, despite multi-product customers being materially more valuable.

76.9%

of customers held one product

1.85×

more revenue from customers with a second product

2.25×

higher AUA for multi-product customers

How might we encourage more customers to take a second Moneybox product, earlier in their journey?

Problem

Existing cross-sell journeys largely promoted products in isolation.

Customers could understand what a Cash ISA or Lifetime ISA did individually, but there was little context around why opening a second product could help them make progress towards a broader financial goal.

Insight

Would outcome-led bundles make taking a second product feel more relevant?

We believed customers would be more likely to open a second product if complementary accounts were framed around a shared financial outcome, rather than presented as standalone cross-sell offers.

For example, instead of recommending a Cash ISA after someone selected a Lifetime ISA, we introduced a First-time Buyer bundle, positioning it as a way to not only save for your deposit, but for other home-buying costs, such as furniture and fees.

Experimentation & strategy

Rather than build a full two-product registration journey upfront, we tested the proposition in three progressive phases.

Each phase answered a different question:

Phase 1

Is there appetite for bundles?

We started with a lightweight fake-door test. This allowed us to validate demand before investing in a more complex registration flow.

After selecting their first product, customers were offered a relevant complementary bundle. To keep scope low, customers still registered for their original product first. If they chose a bundle, they were prompted to open the second product later through an onboarding hero module.

Results

30%

of customers selected a bundle when shown one

68%

of those customers went on to open the second product post-reg

All three bundles drove higher cross-sell than the existing journey.

Learnings

- Customers were open to a second-product recommendation when it was tied to a clear financial outcome.

- We saw early evidence that bundles could influence which second product customers chose. For example, users choosing the First-time Buyer bundle were more likely to open a Cash ISA, whereas users in the control journey more often selected a Simple Saver.

- This was directional rather than statistically significant, but it suggested that outcome-led framing could help customers understand the role of a second product.

Phase 2

Can we improve cross-sell?

Phase 1 proved that people liked bundles, but there was still a break between choosing one and opening the second product.

We introduced a post-registration screen that allowed customers to continue directly into setting up their second product. Customers who skipped could still return later through the onboarding hero.

Results

+1.9 - 3.8%

Cross-sell increase across the bundle journeys.

Learnings

Customers did not need to be eased into a second product through a separate journey. Once the value of the bundle was clear, they were willing to set up both products in one registration flow.

Phase 3

Will users open two products at once?

In the final phase, we removed the remaining hand-off.

Customers who chose a bundle saw a combined product-detail experience and completed a streamlined registration journey for both products together.

Technical constraints meant customers could only initially fund one product during registration, then fund the second product immediately after entering the app.

Results

+51.4–76.3%

uplift in cross-sell versus the control journey

That means, for every 1,000 cross-sells in the control journey, Phase 3 generated at least 514 additional cross-sells.

Future phase

Increase second product funding

Phase 3 solved the problem of second-product opening, but second-product funding still lagged behind.

Only 44% of customers funded their second product, compared with around 81% in the control experience. This became the next priority: improving funding without losing the stronger cross-sell performance.

Near-term ideas included an immediate funding prompt and post-registration re-engagement. Longer term ideas explored a connected “fund your bundle” experience that could split a single deposit across both products.

I handed over the opportunity area and early concepts; delivery continued after my involvement.

Outcome

Bundles shifted the team’s approach from product-led cross-sell to outcome-led financial planning.

By helping customers understand how products could work together, and progressively reducing friction in the journey, we proved that users were willing to open two products in one registration flow.

The work created a scalable foundation for increasing multi-product adoption, AUA and long-term customer value.

Get in touch

This website is just a little peek into my work. I’ve got plenty more I’d love to yap about – if you’d like to hear it more, let’s chat!